Key takeaways

– Q2 revenue (€42.9m) up 24% year-on-year but only slightly higher than Q2 2021

– Profit after tax down 24% to €3.3m

– Kambi repays €7.5m convertible bond previously held by Kindred Group and repurchases share

– CEO highlights Bally’s as major signing during the quarter

– Kambi share price initially falls 5% after publication of Q2 report

Kambi has reported €42.9m ($47.5m) in Q2 revenue, a 24% rise year-on-year. Compared to Q2 2021, however, this is a growth of just €0.1m, while Kambi’s Q2 operating profit also fell 25% to €3.7m.

Similarly, profit after tax fell 24% to €2.5m, with EBITA acq (which Kambi reported as earnings before interest, taxation and amortisation on acquired intangible assets) falling 4% to €5m.

EBITDA was up 11% to €12.9m. But earnings per share also fell 24% to €0.083 for Q2.

Kambi, though, was able to confirm it had repaid a €7.5m convertible bond previously held by Kindred Group, while it also repurchased 381,476 shares for a total of €7.2m.

For H1, Kambi’s revenue grew 22% to €86.9m, EBITA acq was 16% down, at €10.8m, while operating profit fell 33% to €12.2m; profit after tax dropped 34% to €8.8m, with H1 EBITDA rising 1% to €25.7m.

Kambi CEO Kristian Nylén commented: “During the quarter we delivered strong revenue growth of 24% year-on-year, driven by new customers, the addition of Shape Games and a high operator trading margin.

“Operator turnover growth of 4% was not as strong as revenue, impacted by rising foreign exchange headwinds, the dampening effect of a high trading margin and Penn Entertainment’s year-on-year decline in US market share.”

Bally’s

Given the previous loss of DraftKings as a key customer for Kambi – and the aforementioned Penn, which will transition away from Kambi in 2024 – Nylén was keen to emphasise the signing of Bally’s as an operator partner in Q2.

He explained: “From a commercial perspective, we were delighted to welcome Bally’s Corporation to the Kambi network in Q2. As we further solidify our market leadership position, this partner win is a major milestone for the business and comes on the back of our flexible product strategy.

“As one of the world’s leading gaming operators, Bally’s commands strong brand recognition, a large customer database and expansive global footprint that has the potential to open up significant opportunities for Kambi in both the US and beyond.”

The CEO also gave mention to Q2 renewals with BetPlay, LeoVegas and Paf.

Q2 breakdown

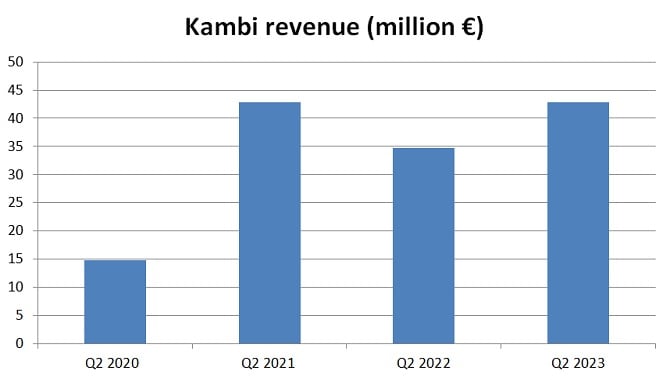

Revenue

As we can see, Kambi’s Q2 revenue of €42.9m represents a significant year-on-year improvement. Compare it to Q2 2020’s €14.8m and it paints a picture of exceptional growth over time.

However, the p is just €0.1m ahead of Q2 2021, when Kambi enjoyed a stellar quarter and generated €42.8m – which was followed by a 19% fall for Q2 2022.

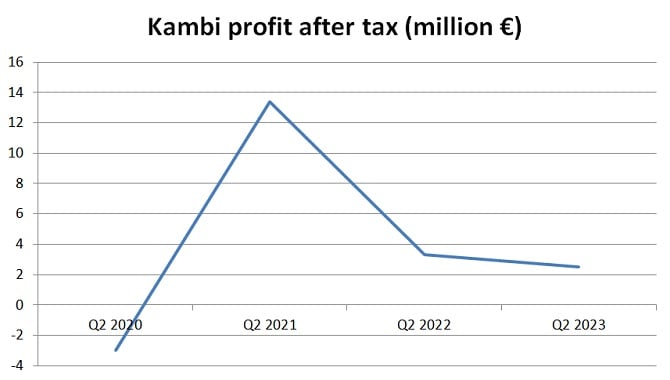

Q2 profit v loss

It is a similar story for the sports betting supplier in terms of profit after tax. Q2 2020 represented Kambi’s weakest recent Q2, when it lost €3m; this was then followed by its best Q2 p in recent years, when it made €13.4m.

But that number fell to €3.3m for Q2 2022. And, while Kambi was still profitable after tax for Q2 2023, the provider fell again in this category – dropping 24% to €2.5m.

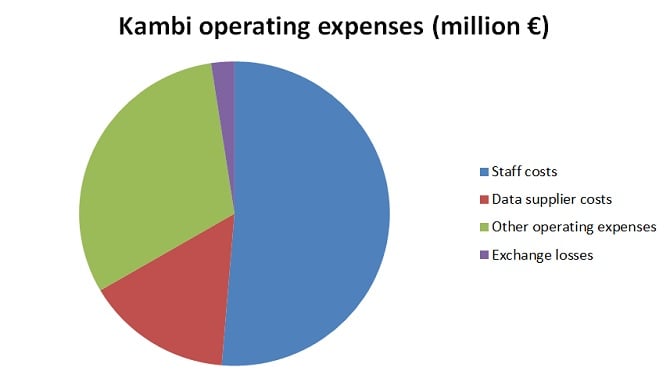

Q2 operating expenses

A breakdown of Kambi’s Q2 operating expenses shows staff as the biggest single cost to the company (at €15.4m).

For Q2, exchange losses also cost the company almost €1m (€727,000). Payments to data suppliers also totalled a sizable €4.6m for the period, while ‘other operating expenses’ amounted to €9.3m.

Kambi’s share price fell 5% immediately after the publication of its Q2 report, from around SEK 198 ($19) to SEK 188; it then rebounded slightly to SEK 191.